![]()

Hyperlipidemia Drug Market to Grow from USD 26.19B in 2026 to $35.82B by 2035-By Rising Global Dyslipidemia Prevalence, Updated Clinical Guideline LDL-C Targets

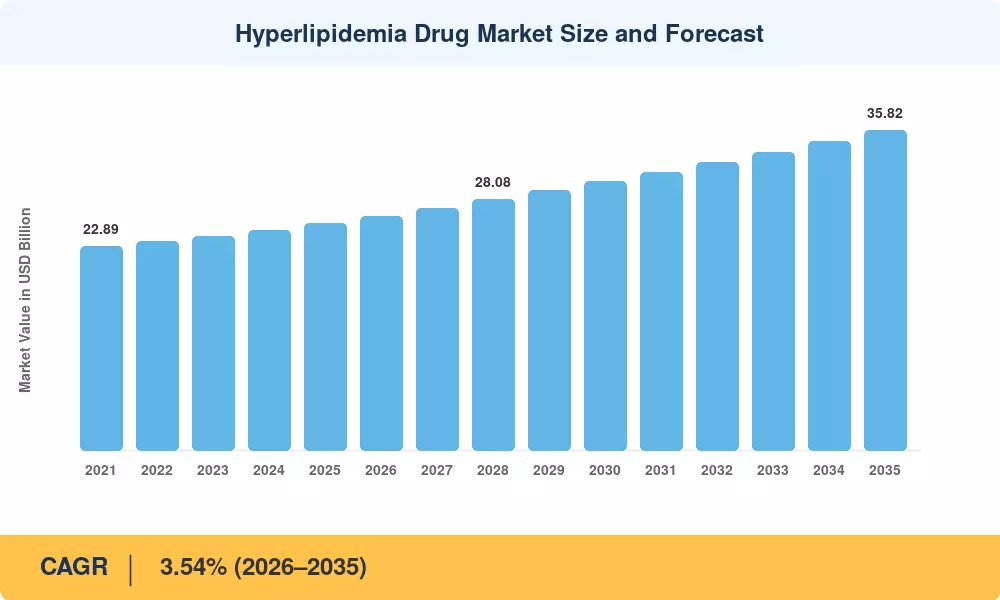

NY, CA, UNITED STATES, July 7, 2026 /EINPresswire.com/ — As per Market Research Future, the global Hyperlipidemia Drug Market size to reach USD 35.82 Billion by 2035 from USD 26.19 Billion in 2026, at a CAGR of 3.54% during the forecast period 2026–2035. The market base was estimated at USD 25.38 Billion in 2025.

The 3.54% CAGR—anchored by structural cardiovascular prevention demand rather than discretionary healthcare spending—is driven by three converging forces: the expanding global burden of dyslipidemia now affecting more than 2.1 billion adults, updated ACC/AHA and ESC/EAS treatment guidelines that continue to lower recommended LDL-C thresholds and push payer systems toward broader coverage of branded and biologic lipid-lowering therapies, and the therapeutic shift from legacy oral statins toward injectable PCSK9 inhibitors, small-interfering RNA medicines such as inclisiran, and next-generation small molecules that address adherence limitations and statin intolerance. The Hyperlipidemia Drug Market is no longer a commoditized generic volume play—it sits at the intersection of precision medicine, outcomes-based contracting, and population health strategy.

National governments and multilateral health organizations are amplifying this momentum. The WHO notes that cardiovascular conditions claim an estimated 17.9 million human lives globally each year, underscoring the demand for durable therapeutic options. China’s Healthy China Initiative accelerates early detection rates across primary care networks, while India’s Ayushman Bharat expands lipid screening into rural health centers.

Request A Free Sample: https://www.marketresearchfuture.com/sample_request/30007

Key Market Trends & Growth Drivers

Rising Global Dyslipidemia Prevalence

World Heart Federation and WHO data indicate that raised total cholesterol affects approximately 39 percent of adults globally. Urbanization, sedentary lifestyles, and dietary shifts expand this patient pool. Government prevention frameworks, such as China’s Healthy China Initiative, accelerate early detection rates across primary care networks, translating large diagnostic baselines into active medical treatment patient cohorts. Each percentage point of diagnosed dyslipidemia prevalence gain translates into measurable prescription volume, and the chronic disease management paradigm embedded in cardiovascular prevention makes this driver structurally durable through 2035.

Updated Clinical Guideline LDL-C Targets

The European Society of Cardiology updates recommend strict lipid targets below 55 milligrams per deciliter for the highest risk patients. Concurrently, international medical guidance endorses nonstatin add-on therapies if thresholds remain exceeded. These tightened clinical requirements expand the eligible patient base for advanced therapies, driving specialty medication utilization and increasing global total prescription script volume. The 2022 expansion of guideline-recommended LDL-C targets in major markets created a structural biologic tail, supporting premium-priced PCSK9 inhibitor and siRNA demand that generic statin regions cannot match.

Biologic and siRNA Therapy Adoption

Clinical data published by the National Institutes of Health indicates that small interfering RNA therapies provide up to 50 percent mean reduction in bad cholesterol. This twice-yearly subcutaneous dosing schedule addresses adherence limitations common to standard daily oral regimens, validating advanced long-acting biological therapies as highly viable tools for future therapeutic market development. The proliferation of injectable biologics and semi-annual siRNA dosing regimens has lowered barriers to adoption in specialty pharmacy and physician-administered settings, though payer access restrictions continue to position many biologics as step-therapy options. Investment activity reflects this shift: industry transaction records show that between 2022 and 2024, the total amount of venture and pharmaceutical license deals aimed at next-generation lipid modulators exceeded USD 4.7 billion.

Ask for Customization: https://www.marketresearchfuture.com/ask_for_customize/30007

Market Segment Insights

BY DRUG CLASS

Statins: Dominant segment with ~72.5% revenue share in 2025. Reflecting decades of entrenched guideline recommendations and low-cost generic availability that drives massive prescription volumes. Atorvastatin alone accounts for roughly 35% of all lipid-lowering prescriptions globally, with rosuvastatin capturing an additional 22%. Lipitor and Crestor anchor this segment. The drug class’s dominance, however, is primarily volume-driven; value growth increasingly originates from the PCSK9 inhibitor and siRNA segments.

PCSK9 Inhibitors: Fastest-growing drug class at 4.0% CAGR (2026–2035). Evolocumab and alirocumab generated combined global sales exceeding USD 4.2 billion in 2024. Improved payer access—driven by cardiovascular outcome trial data demonstrating significant MACE reductions—has expanded the commercially viable patient population beyond familial hypercholesterolemia into broader secondary prevention cohorts. As formulary consolidation around PCSK9 agents accelerates, manufacturers able to demonstrate real-world cardiovascular event reduction capture a disproportionate share.

Bempedoic Acid & Ezetimibe: Growing segment; oral non-statin alternatives that avoid muscle-related side effects. Fixed-dose combinations of these agents are gaining formulary traction for the estimated 10–15% of patients who cannot tolerate statins. Nexletol and Zetia anchor this segment.

siRNA Therapies: Emerging segment; inclisiran (Leqvio) represents the first-in-class siRNA lipid-lowering agent with twice-yearly dosing. The NHS England rollout targeting 300,000 high-risk patients signals population-level adoption potential.

Others (Fibrates, Bile Acid Sequestrants, Antisense Oligonucleotides): Niche demand; primarily combination therapy and add-on prescribing for mixed dyslipidemia and statin-intolerant populations.

BY INDICATION

Primary Hyperlipidemia: Dominant indication with ~48% of demand in 2025, representing roughly USD 12.18 Billion. Driven by familial hypercholesterolemia and polygenic hyperlipidemia diagnoses that require lifelong pharmacologic management. Each percentage point of diagnosis rate gain translates into measurable prescription volume.

Cardiovascular Disease Prevention: Fastest-growing indication segment. The expansion of PCSK9 inhibitor labels into secondary prevention and the WHO framework calling for at least 50 percent of eligible high-risk individuals to receive preventive drug therapies are converting a treatment-dominated market into one with a structural prevention tail.

Secondary Hyperlipidemia: USD 4.87 Billion in 2025; diabetes, nephrotic syndrome, and hypothyroidism-associated dyslipidemia drive add-on therapy demand.

Mixed Dyslipidemia: Growing segment; combination fixed-dose therapies targeting multiple lipid fractions simultaneously are gaining formulary preference.

BY ROUTE OF ADMINISTRATION

Oral: Dominant delivery route with 60.6% of the Hyperlipidemia Drug Market in 2025, reflecting the dominance of statin and ezetimibe prescriptions. The sheer volume of daily oral statin prescriptions—over 90% of which are generic—anchors this segment.

Injectable: Fastest-growing route at 4.8% CAGR. Propelled by the adoption of injectable biologics and semi-annual siRNA dosing regimens. Inclisiran uses a buy-and-bill physician-administered model with twice-yearly dosing, bypassing specialty pharmacy networks entirely. This contrasts with monthly self-injected PCSK9 antibodies distributed through retail and mail-order channels.

Transdermal: Emerging segment; patch-based delivery technologies for statins and combination therapies are in early-stage development.

BY DISTRIBUTION CHANNEL

Retail Pharmacies: Largest segment at ~45.8% share in 2025. Walk-in dispensing for chronic oral prescriptions remains the primary dispensing point, handling the majority of statin and fibrate prescriptions.

Hospital Pharmacies: USD 7.24 Billion in 2025, serving as the initiation point for inpatient lipid management and specialty infusion centers for PCSK9 inhibitor first administration.

Online Pharmacies: Fastest-growing channel at 5.2% CAGR. Digital health platform expansion, telehealth prescribing, direct-to-consumer platforms, and subscription refill models reduce friction for patients managing long-term lipid therapy. Adoption has grown 28% annually since 2022, particularly among commercially insured populations under 65.

Specialty Pharmacies: Growing channel for biologic PCSK9 inhibitors and siRNA therapies; integrated with outcomes-monitoring and adherence-tracking services.

Read Detailed Insights: https://www.marketresearchfuture.com/reports/hyperlipidemia-drug-market-30007

Regional Outlook

North America — Dominant Market (~42.0% Share, 2025)

The United States generates approximately 85.2% of North American Hyperlipidemia Drug Market revenue, driven by high per-capita specialty drug spending and a well-established PCSK9 inhibitor prescribing ecosystem. CMS’s 2025 Medicare Part D redesign capped out-of-pocket costs at USD 2,000 annually, improving biologic access for seniors with familial hypercholesterolemia. Reimbursement breadth and outcomes-based contracting support premium-priced PCSK9 inhibitor and siRNA demand that emerging markets cannot match.

Canada contributes through provincial formulary alignment, while Mexico is growing on IMSS lipid screening expansion under the PREVENIMSS+ preventive care platform, contributing USD 0.56 Billion in 2025. North America’s leadership rests on specialty pharmacy infrastructure depth and the structural biologic segment created by expanded cardiovascular outcome trial data and payer risk-sharing agreements.

Europe — Second Largest (~28.1% Share, 2025)

Europe’s Hyperlipidemia Drug Market reflects divergent national strategies—Germany leads regionally with AMNOG outcomes-based pricing for PCSK9 agents at 3.8% CAGR, while the UK historically used selective hospital targeting before broadening coverage through the NHS inclisiran population health rollout targeting 300,000 patients by 2026. France contributes 17.4% of regional share through Haute Autorité de Santé biologic endorsement.

Italy contributes USD 0.98 Billion on AIFA therapeutic plan compliance incentives. Harmonization pressure from EMA centralized approval pathways is gradually narrowing these differences, lifting baseline demand across the region. The Nordic countries are growing at a steady pace on integrated electronic health record prescribing. Spain contributes through SNS cardiovascular prevention strategy at 3.2% CAGR. Russia holds a smaller share through essential medicines list inclusion.

Asia-Pacific — Fastest-Growing Region (5.4% CAGR, 2026–2035)

Asia-Pacific is the engine of the Hyperlipidemia Drug Market. China holds the largest regional share with 38.5% of regional revenue, its centralized drug procurement system having negotiated PCSK9 inhibitor prices down by 60–80% in 2024, dramatically expanding volume access while compressing per-unit revenue. India is growing at 5.8% CAGR on the back of Ayushman Bharat lipid screening rollout into rural health centers.

ASEAN economies show steady growth as rising NCD burden and insurance penetration converge. Japan contributes USD 1.62 Billion through PMDA accelerated approvals for novel mechanisms. South Korea is growing at 4.9% CAGR on HIRA coverage expansion for combination therapies. The rest of Asia-Pacific is growing on improving pharmaceutical supply chains. The region’s combined contribution anchors the global volume base for statin and biologic demand.

Middle East & Africa — Emerging Opportunity (2.7% CAGR, 2026–2035)

The Middle East & Africa carries the widest treatment gap and therefore the steepest long-term opportunity. Saudi Arabia leads the region with Vision 2030 NCD reduction programs including mandatory cardiovascular risk screening for adults over 40, contributing 31.8% of regional share. The UAE contributes through Dubai Health Authority preventive screening at 3.5% CAGR.

South Africa is growing at a solid pace on private sector-led specialty prescribing, contributing USD 0.19 Billion. Egypt is growing at 2.9% CAGR through universal health insurance rollout. The rest of the region is growing steadily on variable healthcare infrastructure and NCD awareness campaigns. Generic statin access gaps remain a restraint—WHO estimates that undiagnosed dyslipidemia in sub-Saharan Africa exceeds 60% of the adult population in challenging regions.

South America — Growing Presence (USD 1.78 Billion, 2025)

Brazil anchors South America’s Hyperlipidemia Drug Market at ~62.4% of regional revenue, with its Unified Health System (SUS) providing free statin and fibrate access to qualifying patients, providing a stable demand floor that smooths regional forecasts. Argentina contributes through PAMI cardiovascular drug coverage at 3.1% CAGR.

The rest of South America is growing steadily on improving primary care access. South America’s procurement runs largely through public health system statin rollout programs. Regulatory modernization through ANVISA’s expedited review pathway has shortened biologic approval timelines by roughly 18 months, positioning Brazil as the region’s first market for novel lipid-lowering agents.

Competitive Landscape and Recent Developments

The Hyperlipidemia Drug Market is moderately concentrated, with an estimated Herfindahl-Hirschman Index in the 1,200–1,500 range and the top five companies holding roughly 55–62% of global revenue. Concentration is highest in high-income segments where regulatory and clinical evidence barriers are steep; the generic statin tier is highly fragmented as regional manufacturers compete on price. Competitive intensity is heightened by looming patent cliffs on key branded statins and the approaching biosimilar window for monoclonal PCSK9 antibodies.

The competitive landscape is stratified between volume leaders dominating generic statin prescriptions, biologic innovators capturing specialty pharmacy share, and precision-medicine players targeting statin-intolerant and familial hypercholesterolemia populations.

KEY COMPANIES AND RECENT MILESTONES

Pfizer Inc. (2024–2025): Maintains leadership through the Lipitor franchise and generic atorvastatin dominance, commanding ~12–16% of global Hyperlipidemia Drug Market revenue. Volume leadership through entrenched first-line guideline positioning offsets biologic pricing compression in specialty segments.

Amgen Inc. (2024–2025): Evolocumab (Repatha) anchors a strong PCSK9 monoclonal antibody franchise, holding ~8–12% of global revenue. The company benefits from the structural biologic tail created by cardiovascular outcome trial data and expanding secondary prevention labels.

Sanofi / Regeneron (2024–2025): Alirocumab (Praluent) anchors a cardiovascular outcomes-driven positioning, holding ~7–11% of global revenue. Strong formulary access in Europe and North America supports premium pricing.

AstraZeneca plc (2024–2025): Rosuvastatin (Crestor franchise) anchors a high-intensity statin segment leadership position, holding ~6–9% of global revenue. The company’s emerging-market footprint captures volume growth as diagnosis rates rise.

Future Outlook: 2026–2035

By 2030, real-world evidence and outcomes-based contracting will become the operating system of hyperlipidemia drug reimbursement. Institutional public health networks increasingly leverage real-world clinical registry outcomes to guide national funding frameworks. By tying reimbursement metrics directly to verified lipid reduction targets, public programs optimize long-term healthcare expenditure efficiency. Electronic health record alerts for guideline-concordant prescribing generate granular adherence data that manufacturers and payers can monetize through predictive analytics and formulary-optimization services, creating a new business model layered on top of the core cardiovascular drug franchise.

Oral PCSK9 inhibitors and next-generation small molecules will reframe cost structures by the early 2030s. Clinical trials registered with the National Institutes of Health focus on oral small molecules targeting cardiovascular diseases, which cause an estimated 17.9 million global deaths annually. These oral therapies eliminate injection barriers, expanding baseline clinical delivery models and integrating seamlessly into scalable global primary healthcare infrastructure. As per-patient costs fall with scale and generic entry, the addressable channel widens from specialty clinics to primary care and community health centers, extending advanced lipid-lowering therapy beyond traditional settings.

More Related Research Insights:

https://www.marketresearchfuture.com/reports/smart-inhalers-market-2117

https://www.marketresearchfuture.com/reports/rehabilitation-equipment-market-43440

https://www.marketresearchfuture.com/reports/surgical-lights-market-5803

https://www.marketresearchfuture.com/reports/stem-cell-manufacturing-market-6942

https://www.marketresearchfuture.com/reports/superdisintegrants-market-6663

https://www.marketresearchfuture.com/reports/injectable-drug-delivery-devices-market-1211

https://www.marketresearchfuture.com/reports/nutrigenomics-market-4009

https://www.marketresearchfuture.com/reports/healthcare-staffing-market-12278

https://www.marketresearchfuture.com/reports/veterinary-infusion-pumps-market-7417

https://www.marketresearchfuture.com/reports/sterilization-equipment-market-6397

Larry Wilson

WantStats Research And Media Pvt. Ltd.

+1 855-661-4441

email us here

Visit us on social media:

LinkedIn

Facebook

YouTube

X

Legal Disclaimer:

EIN Presswire provides this news content “as is” without warranty of any kind. We do not accept any responsibility or liability

for the accuracy, content, images, videos, licenses, completeness, legality, or reliability of the information contained in this

article. If you have any complaints or copyright issues related to this article, kindly contact the author above.

![]()

Media gallery